Rainy Season Preparedness Tips for Filipinos

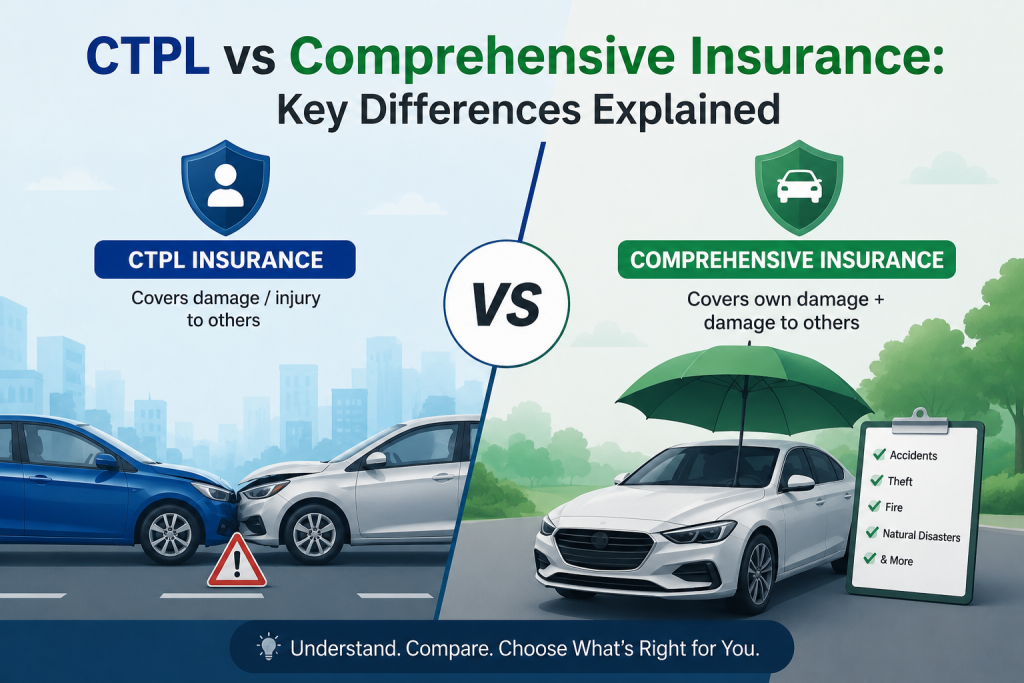

The rainy season in the Philippines brings cooler weather and much-needed rainfall, but it also increases the risk of flooding, road accidents, property damage, and travel disruptions. Every year, heavy rains and typhoons affect thousands of families, businesses, and communities across the country. Preparing before severe weather arrives can help reduce risks, protect property, and improve safety during emergencies. Whether you are a homeowner, vehicle owner, traveler, or business operator, taking proactive steps can make a significant difference when conditions worsen. Understanding Rainy Season Risks The Philippines experiences multiple tropical cyclones each year, many of which bring strong winds, heavy rainfall, and flooding. Common rainy season risks include: Understanding these risks is the first step toward effective preparedness. Prepare Your Home Before Heavy Rains Arrive Homes are often the first line of defense during severe weather. Before the rainy season intensifies, consider: Homeowners should also review Property Insurance coverage to ensure protection remains aligned with current property values and potential weather-related risks. Protect Your Vehicle from Flood Damage Floodwaters can cause significant damage to vehicles, affecting engines, electronics, and safety systems. Vehicle owners can reduce risks by: Drivers should also understand how Motorcar Insurance may help provide financial protection against covered weather-related incidents. Build an Emergency Preparedness Kit Every household should have a basic emergency kit that can support family members during power outages, evacuations, or prolonged severe weather events. Recommended items include: Having supplies ready before a storm arrives helps reduce stress during emergencies. Plan Ahead for Travel Disruptions Heavy rains and typhoons frequently affect transportation schedules. Travelers should: Individuals planning domestic or international trips may benefit from understanding the protection offered by Travel Insurance when unexpected disruptions occur. Prioritize Personal Safety While protecting property is important, personal safety should always come first. Avoid: Families should establish emergency communication plans and identify evacuation routes before severe weather develops. Unexpected accidents can occur during storms and flooding events, which is why many individuals consider Personal Accident Insurance as part of their overall preparedness strategy. Rainy Season Preparedness Is a Year-Round Responsibility Preparedness should not begin when a typhoon is already approaching. Regular maintenance, emergency planning, and risk awareness can significantly reduce the impact of severe weather on homes, vehicles, businesses, and families. Taking small preventive measures today can help avoid major disruptions and financial losses in the future. Final Thoughts The rainy season is a regular part of life in the Philippines, but its challenges should never be underestimated. Flooding, strong winds, and travel disruptions can affect anyone with little warning. By preparing homes, protecting vehicles, assembling emergency supplies, and staying informed, Filipinos can reduce risks and improve their ability to respond during severe weather events. Preparedness is not only about responding to emergencies. It is about building resilience before they happen.